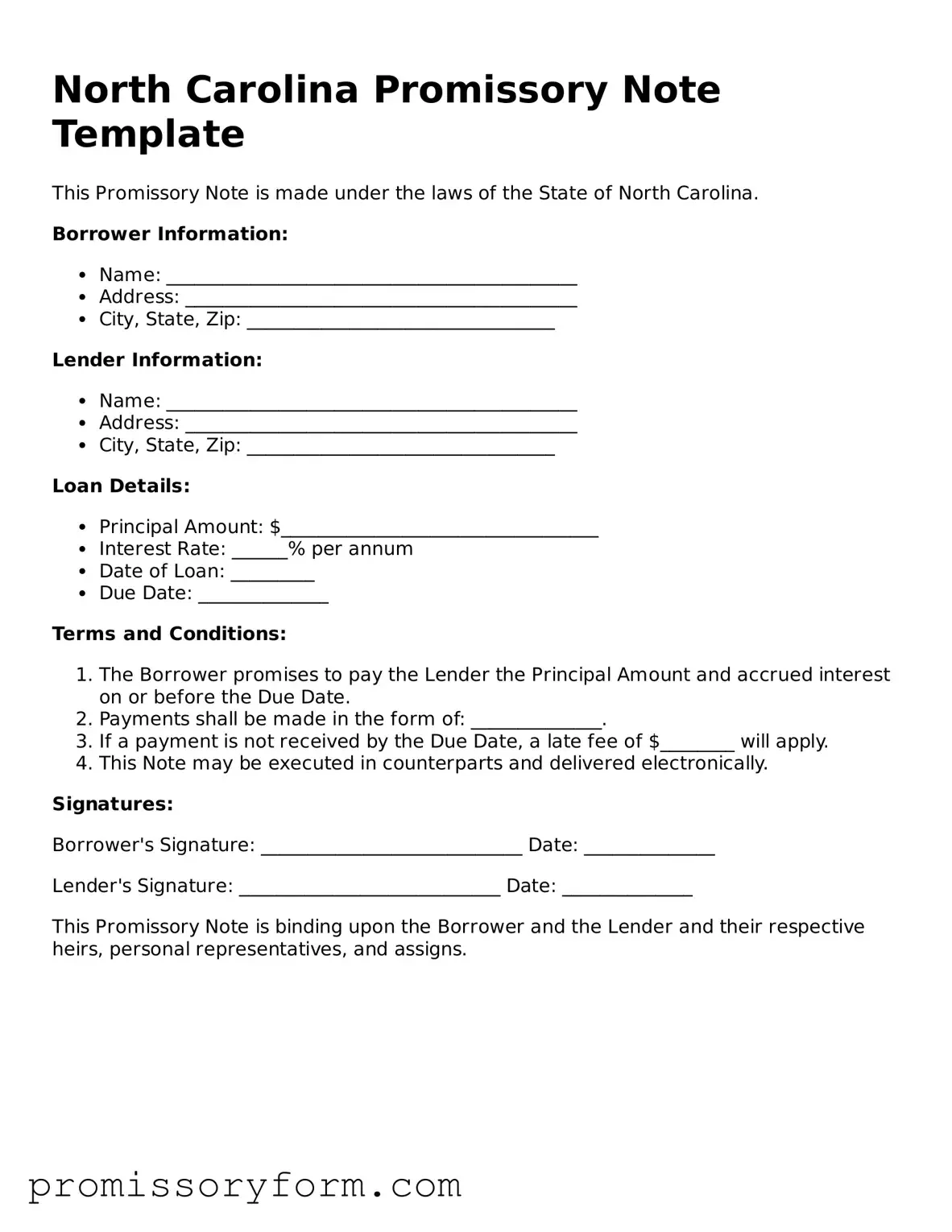

Common mistakes

When filling out a North Carolina Promissory Note, individuals often overlook critical details that can lead to complications later on. One common mistake is failing to clearly specify the loan amount. This figure should be precise and unambiguous. If the amount is written incorrectly or left blank, it can create disputes between the borrower and lender regarding the actual obligation.

Another frequent error involves the terms of repayment. Borrowers sometimes neglect to outline the repayment schedule. This includes the frequency of payments—whether they are due weekly, monthly, or at another interval. Without a clear timeline, misunderstandings may arise, potentially leading to missed payments and penalties.

Many individuals also make the mistake of not including interest rates or failing to specify whether the rate is fixed or variable. Clarity in this area is crucial. If the interest rate is left out or is vague, it can result in confusion about how much the borrower will owe over time. This omission can have significant financial implications.

Furthermore, signatories often forget to date the document. A date serves as a critical reference point for both parties, marking when the agreement was established. If a dispute arises, the absence of a date can complicate matters and affect the enforceability of the note.

Lastly, individuals may overlook the importance of having witnesses or notarization. While North Carolina does not require a promissory note to be notarized, having a witness can add an extra layer of security and legitimacy to the document. This step can help protect the interests of both the borrower and lender in case of future disputes.